Overview

TOKYO—Toshiba Corporation has developed three innovative systems (two high-speed real-time trading systems and one asset management system) that, using quantum-inspired optimization computers, Toshiba’s simulated bifurcation machines (SBMs) (*1-6), detect ever-untargeted trading opportunities through quickly analyzing the complicated correlations between many stock prices in Japanese stock market, and demonstrated the execution capability and effectiveness of those systems.

Analyzing the complicated relations (or collective structure) between many stocks as a core part of new trading/asset management strategies is often mathematically formulated to a quadratic discrete optimization problem classified to be the computationally-hard problem (*7,8), which is difficult to solve in short times with conventional computers. The first and second high-speed real-time trading systems, which detect the trading opportunities by quickly solving quadratic discrete optimization problems with SBMs and then issue buying/selling orders in the Tokyo Stock Exchange, demonstrated that the orders issued are filled at the best bid and ask prices (intended prices) used for the decision-making. This is the world’s first demonstration that the orders based on the quadratic discrete optimization-based decision-making can be filled at the intended prices in a rapidly changing actual market (*9). The third asset management system, thanks to the high acceleration capability of the SBM, evaluated a diversified-correlation portfolio strategy based on a quadratic discrete optimization for an ever-larger-scale universe (tradable stocks) covering approximately 2,000 Japanese stocks and for an ever-longer period (10 years) and eventually demonstrated that the strategy outperforms the major indices such TOPIX and MSCI Japan Min. Vol.

The SBMs are remarkable in terms of being suitable/applicable to real-time, edge/embedded, and/or mission-critical systems (*4,5) in addition to the high acceleration capability. Those pioneering achievements obtained would lead to developing of various derivational systems executing similar strategies but defined by different return/risk measures. The detection and execution of trading opportunities based on the undiscovered correlations amongst many electronically-tradable financial products will contribute to enhance the efficiently (for realizing fundamental/fair prices) and liquidity of the financial markets as a liquidity transfer process to liquidity-depletion products (*10,11,12). The details of the systems were published as three referred journal papers (*13,14,15) in IEEE Access, an open-access journal of the IEEE, on Sep. 18, Oct. 23 and Dec. 12 in Eastern Standard Time (EST), the United States.

A press release summarizing this announcement is available on the Toshiba Corporate Website:

https://www.global.toshiba/ww/news/corporate/2023/12/news-20231215-01.html

Development Background

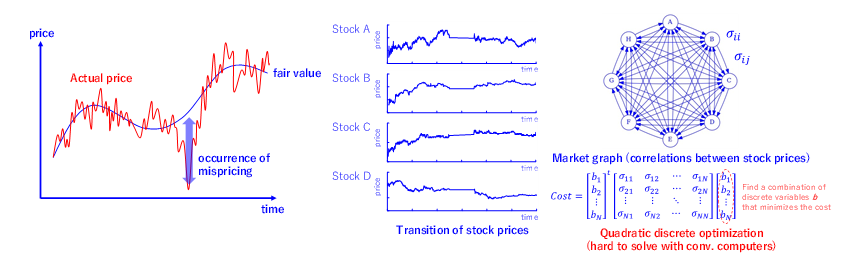

A financial market with high efficiency and high liquidity (an ideal market) is where investors can execute high-volume trading at fair values, at any time without significantly impacting the market prices. Actual prices of individual products (ex. stocks) can be deviated significantly from their fair values (hereinafter "mispricing"), which may force investors to trade at unfavorable prices (Figure 1). The mispricing is caused by some factors such as demand shocks (a sudden unexpected event that dramatically increases or decreases demand for a product) or excessive responses to the news by the media. It is convinced to deduce the fair values and detect the occurrence of mispricing as the deviations of actual prices from the deduced fair values, by analyzing the complicated relationships or collective dynamics among/of the instantaneous prices of many products (*7,8). Those problems to analyze the prices of many correlated products in finance are, when considering minimum transaction lots or other discretenesses of decision variables as realistic constraints, often formulated to a quadratic discrete optimization problem known to be nondeterministic polynomial (NP)-hard in computer science (Figure 1). The computational complexity to solve an NP-hard problem increases exponentially with the problem size (the number of decision variables), making large-scale quadratic discrete optimization challenging.

Toshiba’s simulated bifurcation machines (SBMs), derived from Toshiba’s original quantum computer called quantum bifurcation machines, are quantum-inspired special-purpose digital computers that enable solving quadratic discrete optimization problems at the world highest speed and largest scale (*1,2,3). The SBMs envision the new concept of financial systems featuring quadratic discrete optimization-based decision-making (*4), but those systems need to be validated in the actual market or using the actual historical market data.

Figure 1: Finding the occurrence of mispricing (trading opportunity) through analyzing the correlations between many stock prices, which is formulated as quadratic discrete optimization.

Features of the Technology

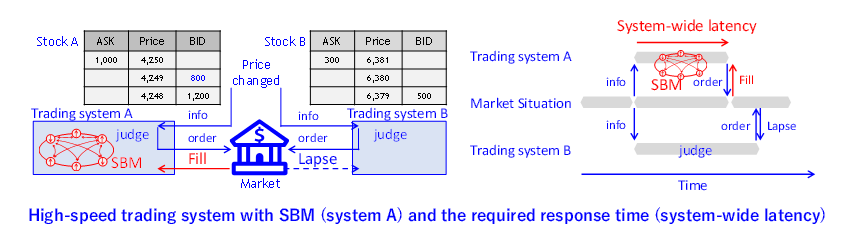

The first and second examples are high-speed real-time trading systems equipped with SBMs that executes trading strategies based on market graph analysis and discrete portfolio optimization, respectively, both of which are typical quadratic discrete optimization problems in the financial field. The quadratic discrete optimization is usually time-consuming to solve, and it had not been demonstrated whether some automated trading systems have a sufficiently low latency (time from market feed arrival to issuance of orders) to execute the quadratic discrete optimization-based strategies (Figure 2). Through the real-time trading records at the Tokyo Stock Exchange, the first and second systems, for the world’s first, demonstrated the execution capability in terms of system latency, i.e., that the orders based on the quadratic discrete optimization-based decision-making can be filled at the intended prices and volumes in a rapidly changing actual market (*13,14).

The system-wide latencies of the first and second systems (including not only the computation time to obtain the solutions of the quadratic discrete optimization problems but also all the latencies of the system components such as communication and the others) are, respectively, 33 and 164 microseconds (the dominant time-component is the computation time of the discrete optimization problem). Those ultra-low latencies are realized by (1) the innovative performance of SBMs in terms of the computation time (*1,2,3), (2) the customization of the SBM algorithm and the system implementation for the proposed strategies (application-specific customization for further speed-up) (*13,14), (3) the co-integration of SBMs with other system components (embedded technology of SBMs) (*13,14).

The first and second systems execute the solver-operation of SBMs more than one every arrival of market feed packet informing the change of the best bid/ask prices. The numbers of the SBM executions per day were typically more than 1 million and 5 million, respectively, for the first and second systems. During the experimental days (totally more than 1,000 hours), no erroneous orders based on wrong calculation were observed, demonstrating the high operational quality of the SBM-based systems.

Figure 2: High-speed real-time trading systems with SBMs that execute quadratic discrete optimization-based strategies, and the required response time.

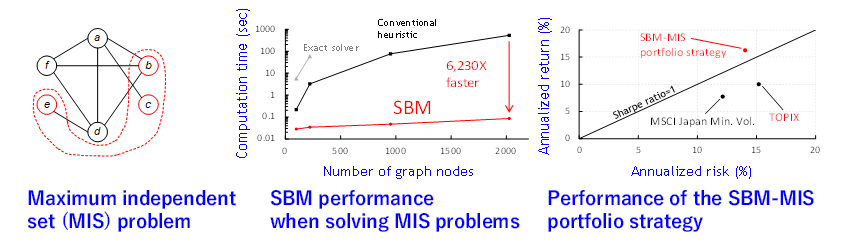

The third example is a development/evaluation system of a diversified-correlation portfolio strategy that selects the stocks to be included in the portfolio based on a maximum independent set (MIS) problem, which is also a typical quadratic discrete optimization problem (Figure 3). Some MIS-based diversified-correlation portfolio strategies had been proposed so far. However, the evolutions of those strategies were limited because of the difficulty of solving the MIS problems (*16,17). Owing to the high speed-performance of the SBM, the third system enables the evolution of a MIS-based portfolio strategy for an ever-larger-scale universe (tradable stocks) covering approximately 2,000 Japanese stocks and for an ever-longer period (10 years). Using the historical data at the Tokyo Stock Exchange and the third system, it was demonstrated, for the first, that a MIS portfolio strategy for a large scale universe shows a good management performance for a long period (*15).

Figure 3: Asset management system based on selection of portfolio through solving maximum independent set (MIS) problems.

Future developments

The first, second, and third systems are all pioneering and practical implementations featuring the decision-making based on quadratic discrete optimization problems which are typical in the finance field, and are expected to lead to the development of various derivatives of those systems. For example, by changing the definition of expected return and/or risk measures, it would be possible to build high-speed trading systems or asset management systems having return-risk characteristics different from those systems. Those systems should apply not only to trading of stocks listed on the Tokyo Stock Exchange but also to that of any other electronically-tradable financial products, and it could be also envisaged to develop new-concept systems based on undiscovered relationships amongst a vast variety of those financial products. Toshiba will endeavor to contribute to the stability and steady growth of financial markets with the cutting-edge technologies.

Acknowledgment

The experiment in the Tokyo Stock Exchange was conducted under a joint project between Toshiba Corporation and Dharma Capital. K.K.

*1: Toshiba Press Release:

https://www.global.toshiba/ww/technology/corporate/rdc/rd/topics/19/1904-01.html

H. Goto et al., “Combinatorial optimization by simulating adiabatic bifurcations in nonlinear Hamiltonian systems,” Science Advances 5, eaav2372, 2019.

https://doi.org/10.1126/sciadv.aav2372

*2: Toshiba Press Release:

https://www.global.toshiba/ww/technology/corporate/rdc/rd/topics/21/2102-02.html

H. Goto et al., “High-performance combinatorial optimization based on classical mechanics,” Science Advances 7, eabe7953, 2021.

https://doi.org//10.1126/sciadv.abe7953

*3: Toshiba Press Release:

https://www.global.toshiba/ww/technology/corporate/rdc/rd/topics/21/2103-01.html

K. Tatsumura et al., “Scaling out Ising machines using a multi-chip architecture for simulated bifurcation,” Nature Electronics 4, pp. 208-217, 2021.

https://doi.org/10.1038/s41928-021-00546-4

*4: Toshiba Press Release:

https://www.global.toshiba/ww/technology/corporate/rdc/rd/topics/19/1910-02.html

K. Tatsumura et al., “A Currency Arbitrage Machine based on the Simulated Bifurcation Algorithm for Ultrafast Detection of Optimal Opportunity,” Proc. of IEEE International Symposium on Circuits and Systems (ISCAS), pp. 1-5, 2020.

https://doi.org/10.1109/ISCAS45731.2020.9181114

*5: Tatsumura et al., “Large-scale combinatorial optimization in real-time systems by FPGA-based accelerators for simulated bifurcation,” Proc. of the 11th International Symposium on Highly Efficient Accelerators and Reconfigurable Technologies (HEART), pp. 1-6, 2022.

https://doi.org/10.1145/3468044.3468045

*6: Toshiba Digital Solutions Corporation, “SQBM+™ (quantum-inspired optimization solutions based on simulated bifurcation machines),”

https://www.global.toshiba/ww/products-solutions/ai-iot/sbm.html

*7: V. Boginski, et al., “Network-based Techniques in the Analysis of the Stock Market,” Supply Chain and Finance, pp. 1-14, 2004.

https://doi.org/10.1142/9789812562586_0001

*8: M. Marzec, “Portfolio optimization: Applications in quantum computing,'' Handbook of High-Frequency Trading and Modeling in Finance, pp. 73-106, 2016.

https://doi.org/10.1002/9781118593486.ch4

*9: Based on examination conducted by Toshiba Corporation

*10: D. Rosch, “The impact of arbitrage on market liquidity,” Journal of Financial Economics 142, pp. 195-213, 2021.

https://doi.org/10.1016/j.jfineco.2021.04.034

*11: E. Gatev et al., “Pairs trading: Performance of a relative-value arbitrage rule,” The Review of Financial Studies 19, pp. 797-827, 2006.

https://doi.org/10.1093/rfs/hhj020

*12: C. Krauss, “Statistical arbitrage pairs trading strategies: Review and outlook,” Journal of Economic Surveys 31, pp. 513-545, 2017.

https://doi.org/10.1111/joes.12153

*13: K. Tatsumura et al., “Pairs-trading System using Quantum-inspired Combinatorial Optimization Accelerator for Optimal Path Search in Market Graphs,” IEEE Access 11, pp. 104406-104416, 2023.

https://doi.org/10.1109/ACCESS.2023.3316727

*14: K. Tatsumura et al., “Real-time Trading System based on Selections of Potentially Profitable, Uncorrelated, and Balanced Stocks by NP-hard Combinatorial Optimization,” IEEE Access 11, pp. 120023-120033, 2023. https://doi.org/10.1109/ACCESS.2023.3326816

*15: R. Hidaka et al., “Correlation-diversified portfolio construction by finding maximum independent set in large-scale market graph,” IEEE Access 11, 2023.

https://doi.org/10.1109/ACCESS.2023.3341422

*16: S. Butenko, “Maximum independent set and related problems, with applications,'' Ph.D. dissertation, University of Florida, 2003.

https://ufdcimages.uflib.ufl.edu/UF/E0/00/10/11/00001/butenko_s.pdf (PDF)

*17: S. Yarkoni et al., “First results solving arbitrarily structured maximum independent set problems using quantum annealing,'' IEEE Congress on Evolutionary Computation (CES), pp. 1—6, 2018.

https://doi.org/10.1109/CEC.2018.8477865